OOH trends 2026: Why outdoor advertising is becoming a global operating system

The billboard is no longer just a billboard. In 2026, the humble poster on the side of a highway has evolved into something far more ambitious: a global operating system for advertising. This is not hyperbole. Walk through any major city and you will see the infrastructure already in place. Screens are everywhere. They are networked, data-driven, and increasingly intelligent. The outdoor advertising industry, long dismissed as a one-way broadcast medium, is quietly building the pipes that will power the next decade of marketing.

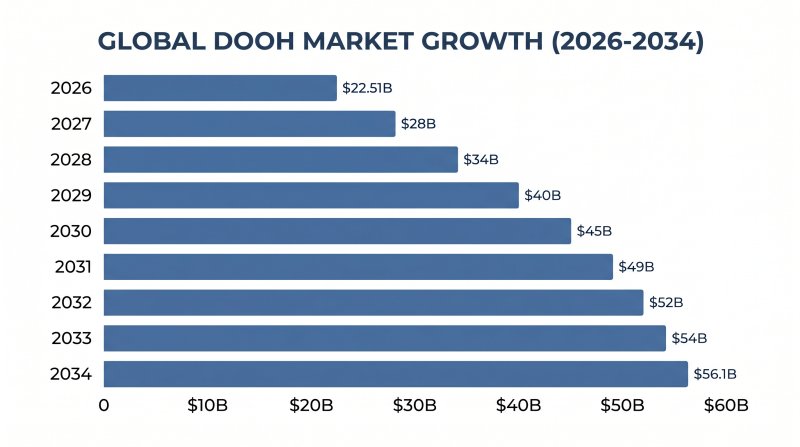

The numbers tell the story better than any narrative can. The global DOOH market is projected to grow from $22.51 billion in 2026 to $56.1 billion by 2034. The compound annual growth rate comes in at 12.09 percent. That is not a modest uptick. That is a fundamental reordering of where brands choose to spend their attention budgets. DOOH will surpass 40 percent of all OOH spend by 2026, which means digital formats will for the first time command a genuine majority of something that was, until recently, almost entirely analog. The global OOH market sits at roughly $40 to $45 billion annually, and within that, the digital slice is the only part growing meaningfully. Traditional static OOH still makes up approximately 65 to 70 percent of the market, but those percentages are eroding fast, with DOOH expanding at 10 to 12 percent annually while traditional OOH clings to roughly 0.7 percent growth.

These figures matter because they signal a structural shift, not a cyclical one. When an industry transforms at these speeds, the brands that understand what is happening early will capture disproportionate value. The ones that treat DOOH as a novelty will find themselves buying remnant inventory at premium prices while smarter competitors own the platform layer.

The shift from locations to liquid audiences

For decades, outdoor advertising operated on a simple logic. You rented a location. The location had traffic. Traffic meant eyeballs. The transaction was about geography, and the measurement was brutally crude. You knew how many cars passed a given billboard on an average day. You had no idea who was in those cars, what they cared about, or whether the message even landed.

That model is not dead. It is becoming irrelevant.

The new OOH operates on audience logic. Instead of buying a specific billboard, advertisers are buying the ability to reach a defined demographic wherever that demographic happens to be in the physical world. The screens themselves become irrelevant as fixed points. What matters is that the system knows where the audience is, and can redirect creative in real time to intercept them. This is what practitioners mean when they talk about liquid audiences. The audience flows through the city, and the advertising system moves with it.

Consider what this looks like in practice. A sports drink brand wants to reach men aged 25 to 40 during afternoon commute hours in cities where temperatures exceed 85 degrees. In the old model, they would identify billboards near gyms and highway exit ramps. In the new model, the programmatic DOOH platform knows that this audience clusters near transit stations, coffee shops, and outdoor recreation areas between 5 and 7 PM, and it automatically adjusts which screens receive the creative based on live conditions. Weather data, transit schedules, foot traffic patterns, and event calendars all feed into the decision. The ad follows the audience, not the other way around.

This shift is being enabled by the rapid expansion of digital screens across public spaces. There are now millions of networked digital displays in airports, transit stations, retail environments, and urban corridors worldwide. These screens were installed for different reasons by different owners, but they are increasingly connected through middleware platforms that allow them to be treated as a single, unified inventory layer. That unification is the technical foundation of the operating system metaphor. Individual screens become nodes in a network. The network becomes the product.

One thing that gets lost in the enthusiasm about liquid audiences is how genuinely difficult this transition is for legacy players. A billboard owner who has spent 30 years building a portfolio of premium highway locations is being told that their core asset, location, is becoming secondary to audience data and algorithmic distribution. That is a real business threat, not a theoretical one. The smart ones are investing heavily in becoming technology companies. The slow ones are hoping it passes.

Programmatic DOOH: From promise to default

Programmatic advertising has been promised as the future of DOOH for well over a decade. The promise always outpaced the reality. The infrastructure was fragmented. The standards were inconsistent. The data integration was clunky at best. Publishers and buyers could not agree on basic measurement definitions. These were legitimate criticisms, and they delayed widespread adoption.

2026 is the year the promise finally becomes the default.

The US DOOH programmatic market is currently valued at approximately $2.2 billion, and global programmatic DOOH ad spending is projected to reach $1.35 billion by 2026. These figures are substantial, but what makes them significant is the trajectory. Programmatic DOOH is no longer a pioneering strategy for early adopters. It is becoming the standard procurement method for media buyers who want flexibility, transparency, and real-time improvements.

The acceleration has several drivers. First, the supply side has consolidated around a smaller number of serious SSPs and DSPs that actually work. The early spread of half-baked platforms that promised programmatic access but delivered frustration has given way to a handful of infrastructure providers that have solved the hard technical problems. Second, the buyer side has matured. Agency traders who cut their teeth on programmatic display and video have moved into leadership roles, and they bring the expectation that DOOH should be bought the same way search and social are bought. Third, and perhaps most importantly, the creative tools have caught up. Flexible creative for DOOH is now accessible to mid-sized brands, not just the largest CPG companies with seven-figure production budgets.

One thing that should not be overlooked in this discussion is the role of creative variability. Programmatic DOOH is not just about buying differently. It is about thinking differently about what outdoor advertising can say and show. A brand that runs the same 10-second loop across 500 screens is using programmatic buying with static creative thinking. The real opportunity is in adapting the message to context. Time of day, weather conditions, nearby retail locations, real-time events, and audience composition should all influence what appears on screen. A coffee brand can show hot beverages on cold mornings and iced options during heat waves. A movie studio can promote different titles based on proximity to theaters where films are opening that weekend. This contextual intelligence is what separates programmatic DOOH from basic automation.

Measurement remains a legitimate concern, and the industry has not fully resolved it. Attribution for physical world advertising will always be imperfect compared to digital channels where every click is tracked. However, DOOH measurement has improved dramatically. Location data from mobile devices, when aggregated responsibly, provides much better audience verification than traditional estimates. Studies consistently show that 80 percent of consumers take action after seeing an engaging OOH ad, which suggests the medium is working even when the causal chain is harder to trace than in digital advertising. The industry is moving toward impression-based measurement standards that will make cross-channel comparison more meaningful, and that shift will accelerate programmatic adoption further.

The 40 percent statistic from agency professionals expecting their clients to increase OOH spending is worth dwelling on. These are not enthusiasts or early adopters. These are professional media buyers who have been through multiple technology cycles and know how to evaluate a channel on its merits. When 40 percent of them are telling their clients to put more money into OOH, something structural has changed in the market.

The sustainability factor

Environmental considerations are reshaping purchasing decisions across every category of business spending, and outdoor advertising is not immune. The traditional OOH model relies heavily on vinyl printing, which is energy-intensive to produce and difficult to recycle. A single large-format billboard print campaign can generate thousands of pounds of waste material. As brands face increasing pressure from stakeholders to demonstrate environmental responsibility, the sustainability profile of different advertising channels is becoming a genuine factor in media planning.

DOOH has a compelling advantage here. A digital screen can display an unlimited number of creative variations without producing physical waste. There are no printing materials, no shipping of panels, no installation and removal labor for each new campaign. The carbon footprint of a DOOH campaign is concentrated in the manufacturing and electricity consumption of the hardware, which is amortized across thousands of hours of content over the screen operational lifetime.

This matters more than it might initially seem. Several major holding companies have committed to achieving net-zero carbon footprints across their operations and supply chains by 2030 or earlier. When your media plan includes thousands of static OOH placements, explaining the environmental impact becomes genuinely difficult. When the same plan uses a network of existing digital screens, the calculation looks quite different. Some networks are now able to provide carbon equivalent data per campaign, allowing buyers to make informed choices and report on the environmental characteristics of their media spend.

There is also an interesting secondary effect worth noting. As more brands shift discretionary spend toward DOOH because of its sustainability profile, the inventory economics improve for publishers who have already made the capital investment in digital infrastructure. This creates a virtuous cycle where better digital inventory availability makes the channel more attractive to more advertisers, which funds further expansion of digital networks. The environmental argument and the commercial argument are reinforcing each other in ways that feel different from previous technology transitions in the medium.

I will say that the sustainability argument for DOOH is real but somewhat overstated by advocates. The electricity consumption of a large digital billboard network is not trivial. The manufacturing footprint of the hardware itself is significant. Calling DOOH a green medium is a relative statement, not an absolute one. But relative to the alternatives, and particularly relative to single-use printed static formats, the case is strong and getting stronger as renewable energy penetrates the grid.

Regional outlook: Who is leading and who is following

The global DOOH market is not uniform. Different regions are at different stages of adoption, and understanding these distinctions matters for any brand planning international campaigns.

North America leads with approximately 33.64 percent of the global market share. This dominance reflects several factors. The United States has an extraordinarily dense network of digital screens, particularly in transit, retail, and urban environments. American media buyers were early adopters of programmatic thinking, which made the transition to programmatic DOOH relatively natural. The US DOOH revenue surpassed $9 billion for the first time in 2024, a milestone that signals how far the market has matured. Canadian and Mexican markets have followed the US trajectory with slight delays, creating a continental bloc that punches well above its weight in terms of innovation and spending.

Europe presents a more fragmented but rapidly evolving picture. Western European markets, particularly the United Kingdom, Germany, France, and the Netherlands, have substantial digital networks and growing programmatic adoption. The regulatory environment in Europe, including GDPR, has created some friction for audience targeting capabilities, but the overall trend is toward greater digitalization and programmatic access. Eastern European markets are earlier in their development curves but are growing quickly as digital infrastructure expands.

Asia-Pacific is perhaps the most interesting long-term story. China has built an extraordinarily sophisticated digital OOH ecosystem, particularly in urban centers, though the measurement and programmatic layers operate differently from Western models due to regulatory and competitive structures. The innovation happening in markets like Japan and South Korea is also worth watching closely. Japan, South Korea, Australia, and Southeast Asian markets are all growing rapidly. The middle class expansion in Southeast Asia alone is creating new audiences that will demand advertising infrastructure, and digital OOH is the natural form factor for these emerging markets.

What this means for international advertisers is that a global DOOH strategy cannot simply replicate a domestic approach across borders. Market structures, measurement standards, and programmatic infrastructure vary so significantly that what works in New York may not translate to Singapore or São Paulo. The brands winning at global OOH are those that have built regional expertise and localized execution capabilities, not those that have attempted to impose a single playbook everywhere.

What this means for advertisers in 2026

If you are a brand manager or media buyer, the implications of this shift are concrete and they are arriving now, not at some distant future date.

First, OOH belongs in your cross-channel mix in a way that it did not five years ago. The measurement has improved enough to justify inclusion alongside digital channels. The programmatic access has lowered the operational barriers to entry. And the audience reach remains genuinely broad in a way that few digital channels can match. OOH is not competing with digital. It is complementing it, and increasingly it is being bought through the same programmatic pipes as everything else.

Second, the way you plan OOH should change. The old model of identifying premium locations and buying them directly is giving way to audience-first planning. Start with the demographic you want to reach, the contexts that matter to them, and the data signals that indicate intent. Then work backward to which screens and which networks can deliver against that brief. This requires a different mindset and different tools, but the results justify the investment.

Third, creative strategy for OOH needs to evolve. Static creative that works on a billboard is not enough anymore. If you are investing meaningfully in DOOH, you should be thinking about responsive creative that changes based on the conditions in which it will be seen. The brands that will win in this space are those that treat DOOH as a data-enabled medium rather than a digital poster.

There is also a talent implication worth noting. The old OOH specialist was a relationship manager who knew which locations performed well and negotiated good rates. The new OOH specialist needs to be comfortable with data platforms, programmatic buying interfaces, and real-time adjustment workflows. This is a real skills gap in the industry, and it is creating opportunities for people who can bridge the traditional media and digital marketing worlds.

FAQ: Programmatic DOOH in 2026

What is programmatic DOOH and how does it differ from traditional OOH buying?

Programmatic DOOH refers to the automated buying and selling of digital out-of-home advertising inventory through software platforms, similar to how programmatic display or video advertising works. Traditional OOH buying involves direct negotiations with publishers, manual placement of orders, and fixed creative run times. Programmatic DOOH allows advertisers to use data and algorithms to target specific audiences, buy inventory in real time, and adjust creative based on context like time of day, weather, or audience composition.

How big is the programmatic DOOH market?

The US programmatic DOOH market is valued at approximately $2.2 billion. Globally, programmatic DOOH ad spending is projected to reach $1.35 billion by 2026. The broader DOOH market is growing from $22.51 billion in 2026 to an estimated $56.1 billion by 2034. That works out to a compound annual growth rate of 12.09 percent.

Why is DOOH growing faster than traditional static OOH?

DOOH is growing at approximately 10 to 12 percent annually while traditional static OOH grows at roughly 0.7 percent. The difference reflects several factors: digital screens offer creative flexibility that static formats cannot match, programmatic buying reduces friction and improves targeting precision, measurement capabilities have advanced significantly, and sustainability considerations are pushing brands away from single-use printed materials.

How is DOOH sustainability different from traditional OOH?

Traditional OOH relies heavily on vinyl printing for each campaign, generating physical waste materials that are difficult to recycle. DOOH eliminates the printing process entirely by using networked digital displays. A single digital screen can display unlimited creative variations over its operational lifetime without producing additional physical waste. This makes DOOH significantly more sustainable than static OOH, particularly for brands with environmental commitments.

What is the outlook for OOH advertising in North America versus other regions?

North America currently holds approximately 33.64 percent of the global DOOH market share, driven by dense digital screen networks and early adoption of programmatic buying. Europe is rapidly digitizing with strong growth in Western markets. Asia-Pacific represents the highest long-term growth potential as middle class expansion creates new urban audiences. No single model works globally, and successful international DOOH strategies require localized execution.

Conclusion

The billboard is not dying. It is being reborn as something more powerful, more measurable, and more integrated into the broader media ecosystem than anyone imagined a decade ago. The global operating system metaphor is not perfect, but it captures something real about how the industry is evolving. Individual screens are becoming nodes in a network. Fixed placements are becoming fluid audience targeting. Static creative is becoming dynamic, context-aware messaging.

For advertisers, the invitation is to stop thinking about OOH as a separate channel with separate rules and start thinking about it as an extension of the data-driven marketing infrastructure you are already building. The brands that figure this out in 2026 will have a meaningful advantage over those that treat it as an afterthought or a novelty. The infrastructure is ready. The question is whether your organization is.

The Outdoor Advertising Association of America reports that digital OOH revenue continues to rise at double-digit rates. Forty percent of agency professionals expect their clients to increase OOH spending. The trajectory is clear. The only question is whether you are planning to be part of it, or whether you are going to spend 2026 wondering why the rules changed.

Ready to Modernize Your OOH Operations?

Join the leading OOH media owners who use AdGrid to automate their quoting, manage inventory, and grow their revenue.